SMM May 15, 2025:

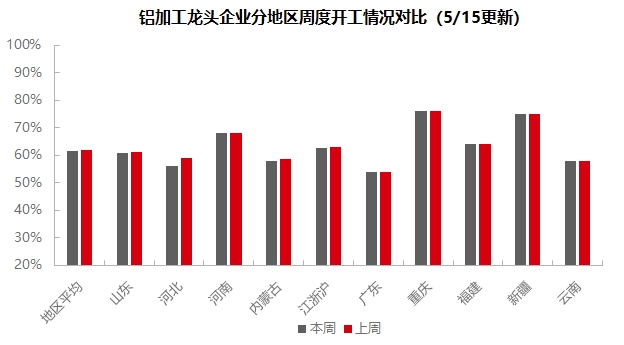

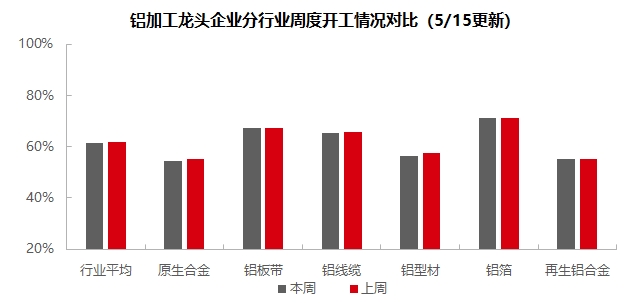

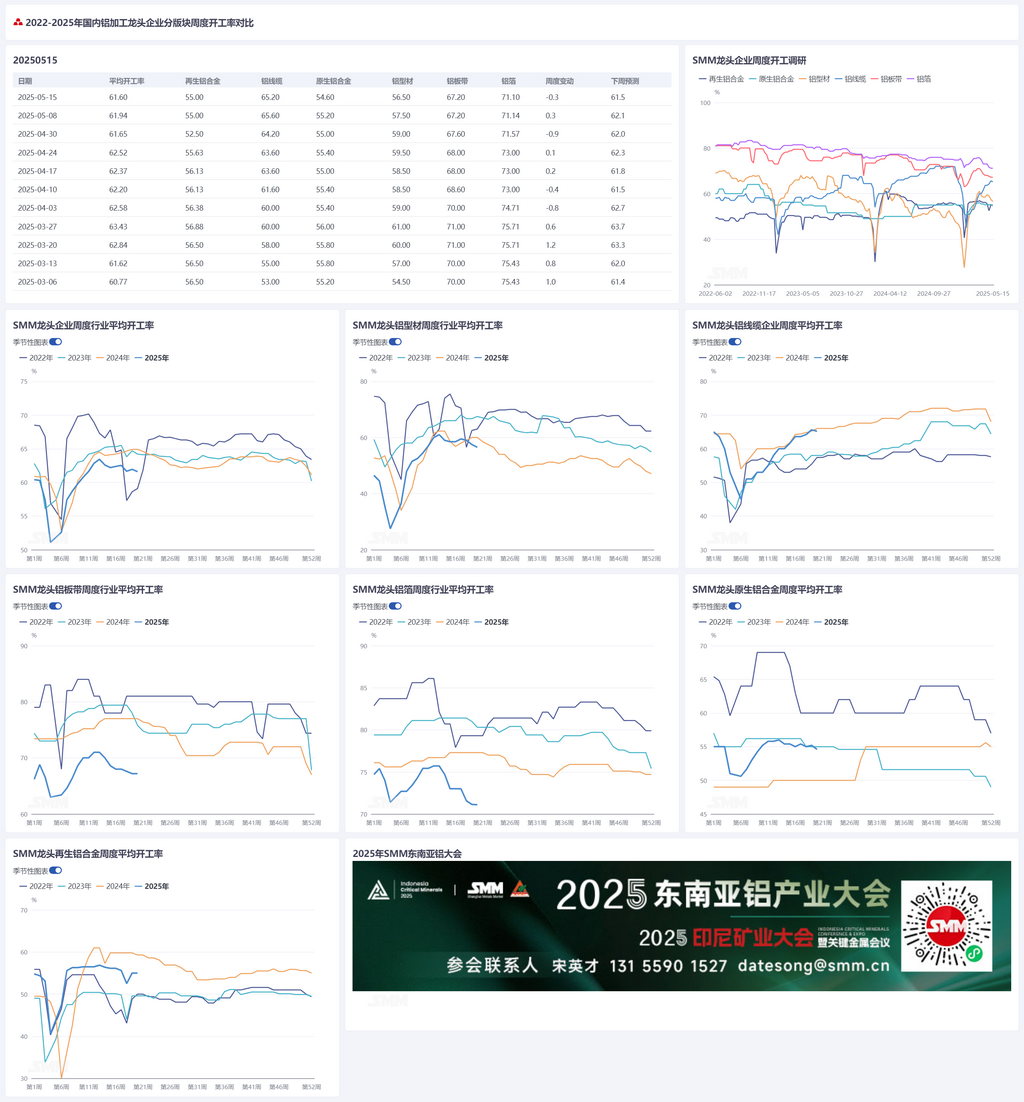

This week, the operating rate of China's leading aluminum downstream processing enterprises fell by 0.3 percentage points WoW to 61.6%, with a divergent pattern across sectors: In the primary alloy sector, downstream consumption in mid-May was constrained by the continuous rise in aluminum prices. Although some enterprises resumed production after maintenance, the impact on overall operating rates was limited. In the export sector, despite the easing of Sino-US relations, large enterprises were still in the order collection phase and remained cautious about rushing to secure export orders. In the aluminum plate/sheet and strip sector, domestic overall consumption remained weak, but the demand recovery in the construction end-user sector had already spread upstream, providing support for operating rates. In the aluminum wire and cable sector, although the rebound in aluminum prices dampened enterprise enthusiasm, driven by the rush-to-meet-deadlines cycle, operating rates remained high. The aluminum extrusion sector showed internal divergence, with the gradual spread of favorable real estate policies boosting orders for some construction extrusion enterprises, while new orders for industrial extrusion continued to be weak. In the aluminum foil sector, stable orders supported operating rates, and attention should be paid to signs of a rebound in export orders in the future. In the secondary aluminum alloy sector, the industry's off-season continued to deepen. Although the easing of tariff policies sent positive signals, the boost to consumption had not yet materialized. SMM expects the operating rate to decline slightly by 0.1 percentage point next week to 61.5%.

Primary Alloy: This week, the operating rate of China's leading primary aluminum alloy enterprises declined, falling by 0.6 percentage points WoW to 54.6%, a decrease of one percentage point from the expectation set last week. In mid-May, some enterprises resumed normal production after completing a 10-day maintenance shutdown, but the impact on the industry's overall operating rate was limited. In mid-May, enterprises within the sample reported that order performance and operating conditions were basically the same as or slightly weaker than those in early May. On the one hand, the continuous rebound and rise in aluminum prices in mid-May had a certain inhibitory effect on downstream consumption of primary alloys, and processing fees performed poorly. Some enterprises chose to produce products such as aluminum billets, which had relatively better processing fees and order performance. On the other hand, although there was an opportunity for easing Sino-US trade relations, it was prudent for enterprises to hold their positions. Moreover, although some enterprises had a need to meet production targets and reach full production by mid-year, the industry's off-season still necessitated maintaining current operating levels. Most enterprises in the industry remained cautious about "rushing to secure export orders." Currently, many large primary aluminum alloy enterprises are still in the order collection phase, and the impact on the operating rates of the aluminum alloy industry is expected to become apparent only after the Sino-US negotiation results become clearer. SMM predicts that the industry's operating rate will maintain a stable but weak trend next week.

Aluminum Plate/Sheet and Strip: This week, the operating rate of leading aluminum plate/sheet and strip enterprises was recorded at 67.2%. On the macro front, the cooling of the Sino-US trade war and the cancellation of reciprocal tariffs had limited impact on the export of aluminum plate/sheet and strip themselves. Firstly, the main export products of aluminum plate/sheet and strip, such as can stock and automotive sheets, are mostly exported in fixed quantities through annual long-term contracts and are not directly exported to the US. Secondly, the existing tariffs on aluminum semis exported to the US have not changed. However, some end-user aluminum finished products, such as home appliances and electronics, are expected to experience a short-term rebound in export activities as companies rush to meet deadlines during negotiation windows. This, in turn, will drive the export-related operating rates of domestic aluminum plate/sheet and strip enterprises. Fundamentals side, domestic overall consumption remains weak, but demand in the construction end-user sector has rebounded, gradually transmitting to the upstream aluminum processing industry, thereby providing some support for the operating rates of the aluminum plate/sheet and strip sector. Overall, driven by the sustained recovery in construction demand and the rush to meet export deadlines in some end-user sectors, the operating rate of aluminum plate/sheet and strip will stabilize temporarily. Attention should be paid to the impact of the implementation of domestic infrastructure policies and changes in the overseas trade environment.

Aluminum Wire and Cable: This week, the operating rate of leading domestic aluminum wire and cable enterprises was recorded at 65.2%, a slight decrease of 0.4% MoM. The main reason is that the rebound in the center of aluminum prices slightly dampened enterprises' enthusiasm for production. However, against the backdrop of a rush to meet deadlines, production can still be maintained at highs, showing resilience. Recently, aluminum wire and cable manufacturers have been producing as planned. Last week, due to the considerable profit margins from order price spreads, there was a stocking demand for raw materials. End-users maintained a steady pace of cargo pick-up, and manufacturers' finished product inventories remained low. In the past week, Sino-US trade relations have eased, but the export business of leading aluminum wire and cable manufacturers has almost no correlation with the US, having no impact on the exports of the aluminum wire and cable industry. These manufacturers still mainly export to Southeast Asia and South American enterprises. Considering enterprises' production schedule expectations and the attractiveness of orders, the industry's operating rate is expected to remain stable.

Aluminum Extrusion: This week, the national operating rate of extrusion enterprises slightly decreased by 1 percentage point MoM to 56.5%. By sector, benefiting from recent real estate policy support, the positive effects of these policies have gradually transmitted to the industry. Infrastructure orders for some leading building materials enterprises in Shandong and central China have continued to rebound, driving up the operating rates of building materials production this week. Meanwhile, despite fluctuations in aluminum prices, enterprises' enthusiasm for raw material procurement has not diminished. In the industrial materials sector, some leading PV frame enterprises reported this week that their operating rates only slightly declined, and they are still producing in an orderly manner according to orders. However, some outsourcing enterprises in east China and Henan reported a severe decline in PV orders, with operating rates maintained at only 40%-50%. An extrusion enterprise in east China that has newly entered the home appliance sector reported that its home appliance capacity is still ramping up. So far, it has not been affected by tariffs based on current orders, and there is no rush to meet export deadlines. This week, the operating rates of automotive extrusion enterprises remained stable, with new orders still sluggish. Some enterprises' attention to aluminum prices surged this week, and they reported that they now need to reduce costs at the source to maintain survival. In terms of exports, a large industrial materials enterprise in east China reported that its export orders remained stable and have not been disrupted by tariffs, mainly because its exports are large items such as high-speed rail, aircraft, and automobiles, which do not suddenly surge in orders due to minor tariff changes. SMM will continue to monitor the actual implementation of orders across various sectors.

Aluminum foil: This week, the operating rate of leading aluminum foil enterprises reached 71.6%. Although orders from aluminum foil producers, including battery foil and brazing foil manufacturers, remain relatively stable, and the production and sales of end-user automakers show growth, providing some support to the overall aluminum foil industry's operating rate, the actual demand from battery manufacturers and automotive parts producers has shown a declining trend, potentially leading to inventory backlogs and subsequent production cuts in the aluminum foil sector. The domestic demand for double-zero packaging foil and air-conditioner foil continues to shrink, with intensified cut-throat competition in processing fees. Overseas, with the removal of reciprocal tariffs in Sino-US trade, there is expected to be a short-term window for negotiations in the home appliance and electronics sectors, leading to a pickup in exports, which in turn will drive the export operating rates of domestic aluminum foil enterprises. It is anticipated that the operating rate of the aluminum foil industry will remain in the doldrums, with a need to closely monitor the inventory digestion progress in the NEV industry chain and the sustainability of the recovery in overseas orders.

Secondary aluminum alloy: This week, the operating rate of leading secondary aluminum enterprises remained stable MoM at 55.0%. The current off-season in the secondary aluminum industry is gradually deepening. Although the easing of tariff policies has sent positive signals to the downstream manufacturing sector, the boost to secondary aluminum consumption has yet to materialize. Additionally, the rapid rise in aluminum prices during the week has triggered a wait-and-see sentiment among downstream players, maintaining a sluggish trading environment in the market. Currently, cost pressures in the industry remain prominent, with the continuous upward trend in primary aluminum prices driving up aluminum scrap prices, while the price increases for alloy ingot finished products have been limited, leading to a further expansion in theoretical losses for the industry. Under the dual pressures of tight raw material supply and weakening demand, the overall operating rate of the secondary aluminum industry showed a downward trend in May, although the operating rate of leading enterprises remained relatively stable during the week.

》Click to view SMM's aluminum industry chain database

(SMM Aluminum Team)